Trends

Let's cut through the automotive hype.

Everyone has an opinion on the future of the car — electric utopia by 2030, self-driving taxis replacing ownership, hydrogen everything. Most of it is written by people tracking stock tickers, not the actual data coming out of factories, dealerships, and research labs.

Here's what's actually happening in 2026 — backed by hard numbers from the IEA, Deloitte's Global Automotive Consumer Study, KPMG's Global Automotive Executive Survey, McKinsey Center for Future Mobility, and other organizations actually measuring the industry — not just reporting on it. Some of these trends are exciting. Some are brutal. All of them are real.

Top automotive industry trends going into 2026:

Let's get into it.

Here's the number the EV bulls didn't want to see: Ford's Model e division burned through $5.1 billion in losses in 2024 — and that's before accounting for the billions more sunk in prior years. This isn't an anomaly. It's the most visible symptom of a structural correction hitting the entire industry.

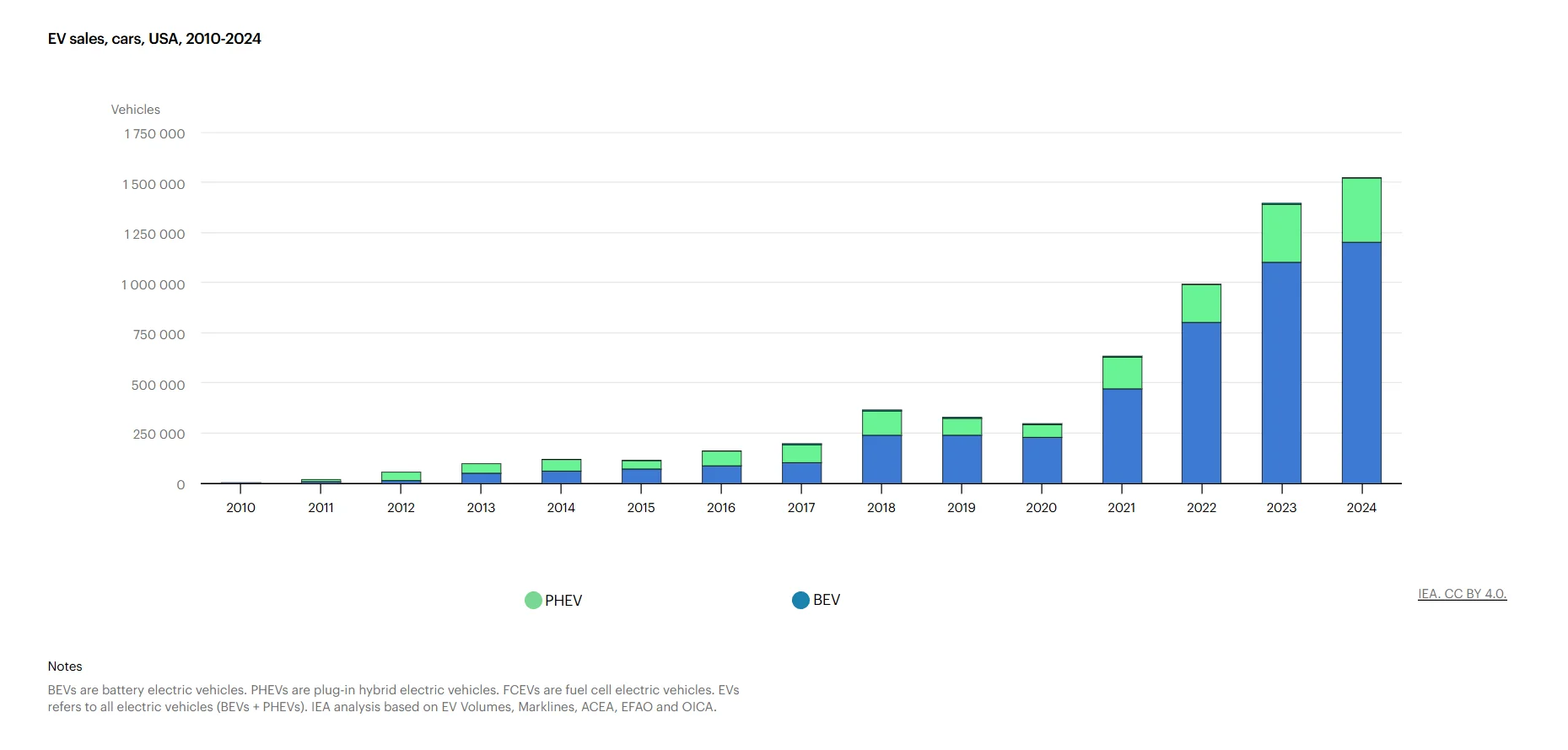

According to the IEA's Global EV Outlook 2025, EV sales growth in the US slowed to about 10% in 2024 — a dramatic deceleration from the 50%+ growth rates of 2021–2023. Consumer hesitation around charging infrastructure, range anxiety, and — most critically — price is real and measurable. Meanwhile, Deloitte's 2025 Global Automotive Consumer Study found that nearly 30% of consumers who had intended to buy an EV switched back to considering a hybrid or ICE vehicle, citing total cost of ownership concerns.

Toyota — widely mocked by analysts for its "slow" EV strategy — is having its moment. Its multi-pathway approach, investing heavily in hybrids while other OEMs went all-in on battery electric, now looks like prescient risk management rather than stubbornness.

Ford Motor Company restructured its EV business in 2024, separating it into a standalone division (Model e) with independent P&L reporting. The transparency exposed just how deep the losses run — and forced the company to pivot its 2025–2026 roadmap toward more hybrids and profitable commercial EVs rather than chasing volume in consumer segments where margin is impossible at current battery costs.

Toyota reported record profits in fiscal 2024, fueled largely by hybrid demand globally. The company's hybrid lineup — including the RAV4 Hybrid, Camry Hybrid, and the Prius revival — is selling at or above MSRP in most markets, in contrast to heavy discounting required to move pure EVs. Toyota's bet on multi-pathway electrification is paying off in real margin terms right now.

General Motors quietly delayed or cancelled multiple EV production commitments in 2024, including the Chevy Silverado EV's planned volume ramp. Instead, the company accelerated investment in plug-in hybrid PHEV variants across its truck and SUV lineup — a direct response to where consumer demand actually is, not where analysts said it would be.

2026 is the year the industry admits the EV transition is a decade-long S-curve, not a cliff edge. PHEVs and HEVs are filling the demand gap, and every major OEM now has a hybrid strategy that's at least as prominent as their BEV strategy. That's not a retreat — it's a recalibration.

Pure EV mandates in the EU and California will continue to pull the long-term direction, but the pace is being reset to match what charging infrastructure and consumer wallets can actually support.

The most important architectural shift in automotive history isn't happening on the factory floor. It's happening in software teams that didn't exist five years ago. Software-defined vehicles (SDVs) — cars where core functions like powertrain tuning, safety systems, and driver assistance are controlled by software that can be updated remotely — are transforming what a vehicle is after it leaves the showroom.

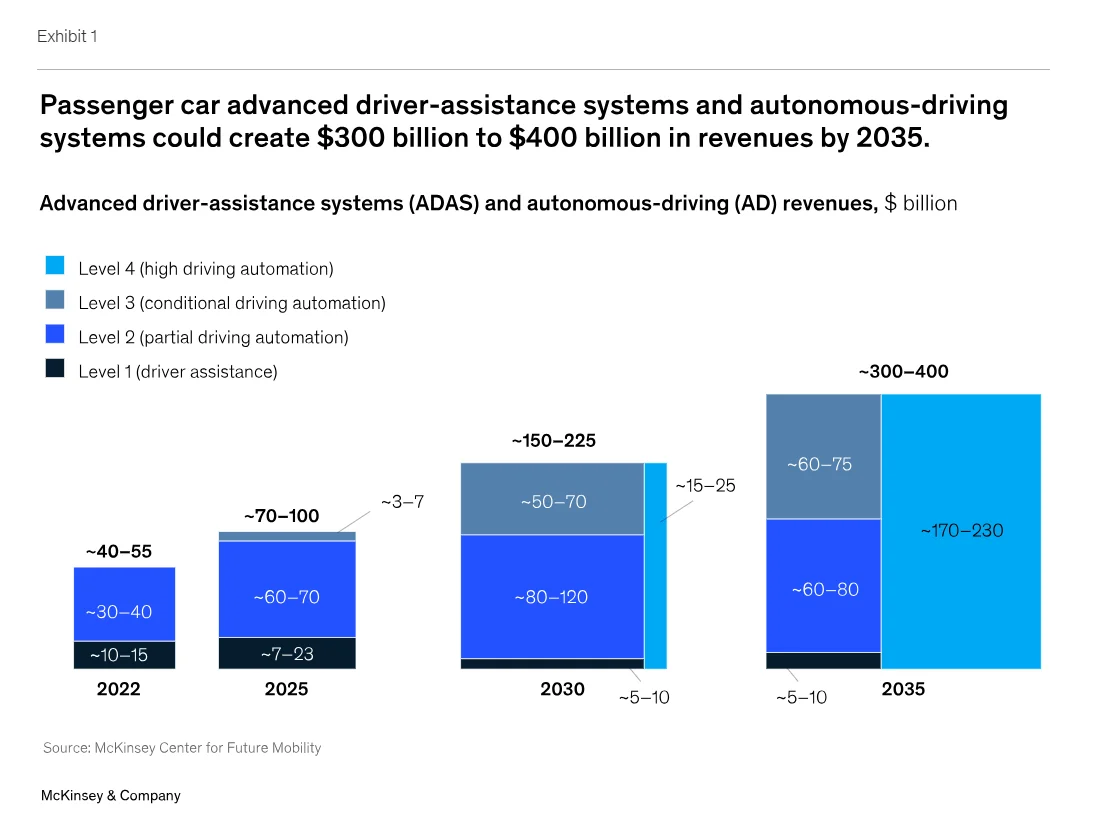

McKinsey's Center for Future Mobility estimates that software and digital features could represent $50 billion or more in annual revenue across the automotive industry by 2030, as automakers convert one-time hardware sales into recurring subscription streams. The traditional model — sell the car, collect the margin, done — is being replaced by a platform model where the sale is the beginning of the revenue relationship, not the end.

Tesla has run this playbook longer than anyone. Over-the-air updates have added features like Track Mode, dog mode, and improved Autopilot capabilities to cars already in customers' driveways — at zero marginal cost to Tesla, at full price to consumers. This is pure software margin: no parts, no labor, no dealer. Tesla's Full Self-Driving (FSD) subscription at $99/month generates recurring revenue from an existing installed base of millions of vehicles.

BMW took a controversial swing with its heated seat subscription model — charging existing owners to unlock hardware already installed in their car. Consumers revolted, and BMW reversed course in several markets. But the underlying economics were sound: the car is the hardware platform, and the monetizable layer is software. BMW's successor approach bundles features into trim tiers, but the principle of software-gated hardware remains.

Volkswagen Group created CARIAD — a dedicated automotive software company — and has committed billions to building the in-house software stack that will underpin all VW, Audi, Porsche, and Seat vehicles. Early execution stumbled badly, delaying multiple product launches. But the strategic thesis is right: OEMs that outsource their software stack to Bosch, Continental, or tech companies will eventually become contract manufacturers rather than brands.

The SDV model flips the automotive profit pool from hardware to software. By 2028, expect most premium vehicles to offer meaningful post-purchase feature unlocks — not just cosmetic, but performance, autonomy, and connectivity features. The automakers that build proprietary software stacks will command premium margins. Those that don't will supply volume to whoever does.

This is the most consequential competitive disruption in the automotive industry in 50 years. BYD outsold Tesla in global battery electric vehicle units starting in Q4 2023 and has not looked back. The Chinese EV industry isn't catching up to Western automakers — in many segments, it has already surpassed them on price, features, and vertical integration.

S&P Global Mobility data shows Chinese automakers — led by BYD, SAIC, and NIO — now hold over 60% of their domestic EV market and are aggressively expanding into Europe, Southeast Asia, Latin America, and Australia. BYD's Atto 3, Seal, and Dolphin models arrive in European markets at 20–35% lower price points than equivalent European or American EVs, with comparable or superior specs.

The response from Western governments has been protectionist: the US imposed 100% tariffs on Chinese EVs, and the EU added tariffs of up to 35.3% on top of existing 10% duties, depending on the manufacturer. These measures are buying time — but they are not solving the underlying cost and technology gap.

BYD is circumventing tariffs by building factories outside China. A plant in Hungary serves the EU market. Plants in Brazil and Thailand are operational. Mexico — strategically positioned under USMCA — was an early target until the US began scrutinizing near-shoring strategies. BYD is playing a long game: tariff walls are temporary, manufacturing presence is permanent.

NIO brings a genuinely different model to markets: battery-as-a-service (BaaS) with swappable battery packs. Instead of waiting 20–40 minutes for a charge, NIO customers swap a depleted battery for a fully charged one in under 5 minutes at dedicated swap stations. NIO has over 2,500 swap stations globally, mostly in China, with European expansion underway. It's a fundamentally different infrastructure bet than fast-charging networks.

CATL, the world's largest battery manufacturer (dominant globally with over 37% market share), is investing in manufacturing capacity in Europe and considering US facilities despite the political headwinds. Whoever controls battery supply controls EV economics — CATL understands this better than almost any company in the world.

The tariff window will narrow. As Chinese OEMs establish manufacturing on multiple continents, the price advantage survives even as the "made in China" label disappears. Western OEMs have roughly 3–5 years to close the cost gap through their own vertical integration, battery investment, and manufacturing efficiency — or face permanent market share erosion in every segment below $50,000.

The US tariff environment in 2025–2026 has forced a supply chain reckoning that makes the COVID disruption look like a dry run. 100% tariffs on Chinese-made vehicles, 25% tariffs on steel and aluminum imports, and the threat of automotive-specific tariffs from multiple trading partners have turned supply chain planning from a 3-year exercise into an 18-month emergency.

According to KPMG's Global Automotive Executive Survey 2025, over 70% of automotive executives ranked geopolitical risk and supply chain disruption as their top concern heading into 2026 — surpassing EV adoption uncertainty for the first time. That's a significant shift. This isn't theoretical risk management — it's active restructuring happening right now, with billions being redirected from product development into supply chain localization.

Ford has accelerated investments in U.S.-sourced battery minerals and domestic battery manufacturing through its BlueOval Battery Park, specifically to meet the Inflation Reduction Act’s (IRA) domestic content requirements and mitigate tariff volatility. While the company is leveraging a technology license from CATL, the goal is to localize production enough to qualify for federal tax credits, though achieving "near zero" Chinese content by 2027 remains a significant industry-wide challenge due to mineral processing dependencies.

Stellantis has aggressively renegotiated supplier contracts to shift sourcing for key components from Asian markets to Mexico and U.S.-based alternatives. Management has publicly acknowledged that while this "near-shoring" strategy involves higher unit costs and potential price increases for consumers, it provides essential protection against fluctuating trade policies and trans-Pacific logistics risks.

General Motors and partner LG Energy Solution have committed more than $7.5 billion specifically to US battery manufacturing, through the Ultium Cells joint venture, with major plants in Ohio, Tennessee, and Michigan. This strategy of deep vertical integration is designed to secure the supply chain. While requiring higher upfront capital than importing, it insulates the company from trade policy volatility and geopolitical risks.

Supply chain localization is expensive — and it raises vehicle prices, which worsens the affordability crisis covered in Trend 7. But the strategic logic is sound. Every major OEM is now making decisions based on a world where trade policy can shift dramatically in 12-month cycles.

Redundancy, domestic sourcing, and regional manufacturing hubs aren't optional anymore — they're the cost of doing business in the 2026 geopolitical environment. For the software platforms helping companies model, manage, and automate this complexity across regions, see our breakdown of the top supply chain software trends in 2026.

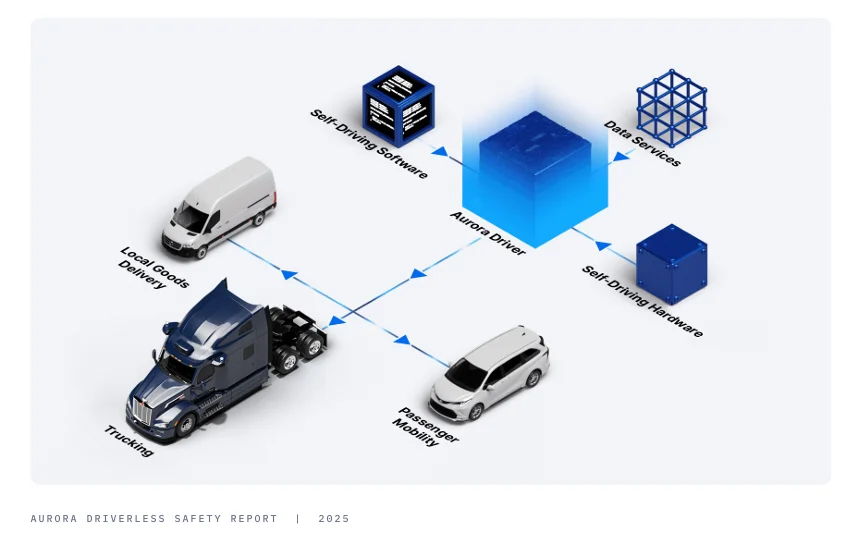

While robotaxi headlines dominate consumer autonomy coverage, the segment where self-driving technology is actually generating commercial revenue is freight. Autonomous Class 8 semi trucks are hauling commercial loads on US highways today — not in a pilot, not in a limited beta, but in operational commercial service.

Aurora Innovation launched commercial driverless trucking operations on the Dallas-to-Houston corridor in 2025 — a significant milestone that received far less attention than it deserved. Aurora's trucks operate without a safety driver, carrying paying freight for commercial shippers. The economics are straightforward and hard to ignore: an autonomous truck can legally operate 22 hours per day with mandatory downtime only for fuel and maintenance, versus an 11-hour limit for human drivers under federal Hours of Service regulations. That's a 100% productivity advantage per vehicle, compounding over a fleet.

The American Trucking Associations reports a driver shortage exceeding 78,000 positions in the US, with demographic trends — aging driver workforce, younger generations less interested in long-haul trucking — making it structurally worse. Autonomous trucking isn't replacing drivers who want to work; it's filling capacity that doesn't exist.

Aurora Innovation has commercial partnerships with FedEx, Uber Freight, and Werner Enterprises. Their Aurora Driver system handles highway operations autonomously; human drivers handle terminal pickups and deliveries. The hybrid model — autonomous on highways, human in complex urban environments — is the commercial bridge that makes the technology viable today without requiring full urban autonomy.

Waymo Via (Waymo's freight division) is testing autonomous semi trucks in partnership with J.B. Hunt Transport Services on the same Texas corridors, with a broader commercial rollout anticipated. Waymo's data advantage from its robotaxi operations — billions of autonomous miles — provides a meaningful head start in safety validation.

Kodiak Robotics is working with the US Department of Defense on autonomous logistics vehicles, in addition to its commercial freight work. Defense applications — supply convoys that expose no human drivers to combat risk — are accelerating government investment in autonomous truck technology that feeds directly back into commercial development.

The autonomous trucking industry has cleared its most important milestone: commercial revenue from driverless operations. What follows is a combination of geographic expansion, fleet scaling, and gradual regulatory clarity. By 2028, autonomous highway freight will be operating in at least 10 US states. The implications for the 3.5 million truck drivers in the US are real and will require serious policy engagement — this is not a "someday" disruption. It is a "right now" one.

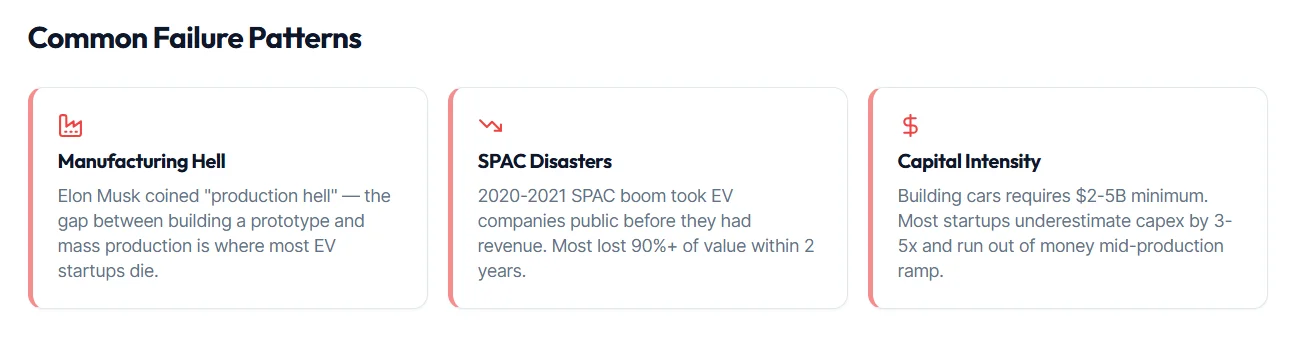

The EV startup boom of 2020–2022 attracted tens of billions in venture and SPAC capital into companies that, in retrospect, were pre-revenue manufacturing businesses with stock prices that implied they'd already won. The bill came due. Fisker, Lordstown Motors, Arrival, Electric Last Mile Solutions, and a dozen smaller players have all filed for bankruptcy or ceased operations. The ones still standing have war stories.

BloombergNEF's Electric Vehicle Outlook 2025 tracks a brutal reality: manufacturing a competitive EV requires $5–10 billion in minimum viable capital to reach meaningful scale — before the first profitable unit. SPACs raised hundreds of millions. They needed billions. The gap was always going to be fatal for most.

What's left is actually more interesting. The survivors — Rivian, Lucid, and a handful of others — have real products, real customers, and real lessons about what it actually takes to build a car company from scratch.

Rivian is the most instructive survivor story. After burning through cash at an alarming rate, the company secured a critical $5 billion investment from Volkswagen Group in 2024 — not just capital, but a technology partnership that validates Rivian's software and electrical architecture. Rivian's R2 and R3 models, targeting mass-market price points around $45,000, represent the company's bet that it can survive the transition from niche to volume production.

Lucid Motors remains alive largely because of continued backing from Saudi Arabia's Public Investment Fund (PIF), which has committed billions to keep the company operational. Lucid's Air sedan has genuine technology leadership — the highest EPA-rated range of any production EV — but converting engineering excellence into commercial scale has proven harder than anticipated.

Fisker serves as the cautionary tale. Despite having a charismatic founder, a striking product in the Ocean SUV, and a capital-light asset-sharing manufacturing strategy, Fisker couldn't solve the downstream problems: service infrastructure, software quality, and customer support at scale. Filing for Chapter 11 in 2024 left thousands of Ocean owners with vehicles that lacked manufacturer support — a reputational disaster for the broader EV startup category.

The EV startup shakeout is not over. Several remaining companies are still operating on runway that requires either profitability or new capital injections by 2027. The consolidation creates real opportunities for traditional OEMs to acquire technology, talent, and manufacturing capacity at distressed prices — watch for strategic acquisitions over the next 24 months.

The winners from this era won't be the companies that raised the most money, but the ones that solved the hardest operational problems.

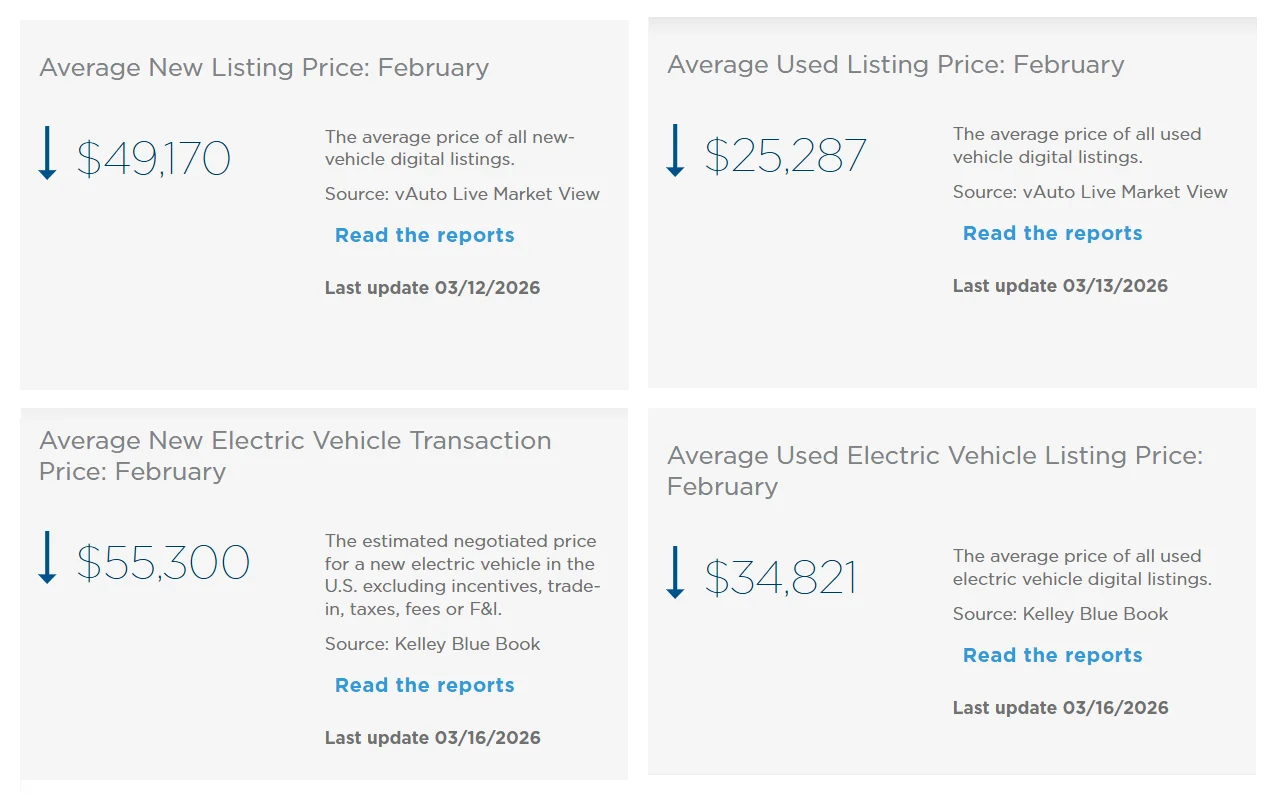

Here's a number that defines the current market: the average transaction price of a new vehicle in the US crossed $50,000 in late 2025. That figure includes both ICE and EV vehicles. It represents a 30% increase from average prices in 2019. Meanwhile, median household income grew at roughly a third of that rate over the same period.

Cox Automotive's Market Insights team tracks an "affordability index" measuring what share of household income a vehicle payment consumes. In 2025, a median-income American household would spend over 20% of monthly take-home pay on a payment for an average new vehicle — a ratio that most financial planners consider unsustainable. Used vehicle prices, which surged during the COVID chip shortage, remain elevated. The bottom of the market has effectively been removed.

Deloitte's Global Automotive Consumer Study found that price is now the #1 barrier to EV adoption — cited by 50% of respondents who expressed hesitation about switching to electric. This is a bigger barrier than range anxiety (31%) or charging infrastructure concerns (29%). The technology works. Consumers just can't afford it at current price points.

Tesla responded to affordability pressure by making its most aggressive price cuts in company history in 2023–2024, reducing Model 3 and Model Y prices by 10–25% in key markets. This helped volume but compressed margins, triggering a brutal earnings reaction. The company's lower-cost Next-Generation Platform — targeting sub-$30,000 pricing — is its answer to the mass market, with production timelines that continue to slip.

GM and Ford are both exploring "value trim" EV variants on existing platforms — stripped-down configurations designed to hit lower price points without requiring new platform development. The challenge is that battery costs still make sub-$35,000 EVs margin-negative at current chemistry and scale.

Hyundai and Kia have positioned themselves as the disruptive leaders of EV affordability. While the standard Ioniq 6 bows out of the US market in 2026 to make room for high-performance variants, the Kia EV6 continues to undercut German luxury and American legacy brands by as much as $10,000. Leveraging their Georgia-based manufacturing hub, these brands have managed to maintain a price-to-feature ratio that few domestic competitors can currently match.

The affordability crisis has a structural solution — declining battery costs — and a timeline problem. Battery costs have dropped roughly 90% over the last decade, but the pace is slowing as easy gains are captured. The next step-change requires solid-state batteries (Trend 9) or fundamentally different manufacturing approaches.

Until then, subscription-based ownership models, longer loan terms (72–84 months is now common), and used EV markets will absorb the pressure that new car pricing can't resolve.

Every car sold in the last five years has some form of driver assistance. Almost none of it qualifies as artificial intelligence in any meaningful sense — it's reactive, rule-based, and brittle. What's entering production vehicles in 2026 is categorically different: AI-native in-vehicle intelligence that learns, adapts, and reasons through novel scenarios with human-like nuance, rather than pattern-matching.

The enabling technology is raw compute. NVIDIA's DRIVE Thor system-on-chip delivers 2,000 TOPS (tera operations per second) — enough to run large language model inference, real-time sensor fusion across cameras and LiDAR, and multiple safety-critical applications simultaneously. This is the compute substrate that makes true AI co-pilots possible. Previous-generation automotive chips operated at 10–30 TOPS; the leap is not incremental.

McKinsey projects that AI-driven personalization and connected services will account for $300–$400 billion in value across the automotive industry by 2030 — a figure that includes data monetization, subscription services, and insurance products built on driving behavior data.

Mercedes-Benz launched DRIVE PILOT, the first production vehicle system to achieve Level 3 conditional automation certified for public roads in Germany and Nevada. The legal significance is enormous: when DRIVE PILOT is engaged, Mercedes accepts liability for the vehicle's actions — a first in automotive history. Drivers can legally take their hands off the wheel and eyes off the road at up to 95 km/h on certified highways.

BMW has integrated an in-vehicle AI assistant powered by large language model technology — allowing natural conversation about navigation, vehicle settings, and even contextual questions about the surrounding environment, processed on-vehicle alongside cloud connectivity. The assistant learns driver preferences over time, adjusting seat position, climate control, and driving mode to individual profiles.

Waymo generates more AI training data from real-world autonomous operation than any other organization on Earth — over 100 million fully autonomous miles driven in public. This data advantage compounds: every mile Waymo drives makes its models slightly better, widening the gap between Waymo and competitors who are working with simulation-heavy, real-world-sparse datasets.

The AI co-pilot category is about to look dramatically different from current ADAS. By 2027, expect production vehicles to offer genuine natural language interaction, predictive routing that learns your patterns, and driver monitoring that can detect fatigue or distraction with medical-grade accuracy.

The regulatory and liability frameworks are the lagging indicator — the technology is already ahead of the legal infrastructure surrounding it. The same large language model and multimodal AI breakthroughs driving this shift are covered in depth in our generative AI trends for 2026.

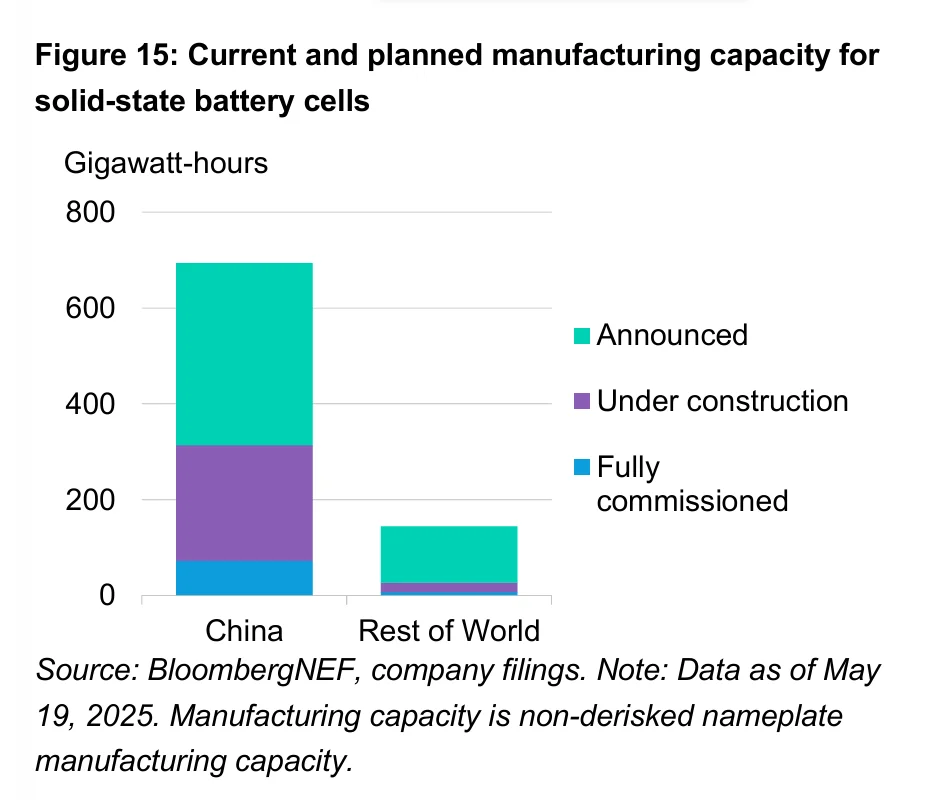

Solid-state batteries replace the liquid electrolyte in conventional lithium-ion cells with a solid material — ceramic, sulfide, or polymer. The theoretical advantages are significant: higher energy density, faster charging, greater thermal stability, and longer cycle life. In practice, getting from laboratory demonstration to mass production has proven harder than almost every timeline predicted.

IEA's State of Energy Innovation 2025 quantifies what's at stake: solid-state batteries could deliver 400–500 Wh/kg energy density versus roughly 250–280 Wh/kg for the best current lithium-ion cells. That translates to either dramatically longer range in the same battery pack size, or the same range in a significantly lighter pack. Either outcome transforms EV economics.

The catch is manufacturing. Solid electrolytes are brittle, difficult to produce consistently at scale, and require entirely new manufacturing equipment and processes. Every company working on SSBs has pushed timelines to the right — repeatedly. But "delayed" is not the same as "cancelled." The physics work. The engineering is solvable. The question is when, not if.

Toyota has staked its entire next-generation EV strategy on solid-state batteries, targeting production vehicles with SSB packs for 2027–2028. The company claims a breakthrough in sulfide-based solid electrolyte durability that resolves a key manufacturing challenge. If Toyota's timeline holds, it would represent the first mass-market SSB vehicle — a significant competitive moat. Toyota also claims its SSB packs will charge from 10–80% in approximately 10 minutes.

QuantumScape, in partnership with PowerCo (Volkswagen Group’s battery unit), successfully began shipping its B-sample lithium-metal solid-state cells (QSE-5) to automotive OEM partners for testing in late 2024. To solve the industry-wide manufacturing scale problem, QuantumScape shifted to a capital-light licensing model in 2024. Under this agreement, QuantumScape provides its proprietary solid-state ceramic separator technology and manufacturing process (known as 'Cobra'), allowing established battery manufacturers to produce the cells within existing or planned gigafactory infrastructure.

Samsung SDI announced in 2024 that it has produced sample solid-state battery cells for automotive customers and is targeting pilot production by 2027. Samsung's involvement is significant: it's an established Tier 1 battery supplier with existing OEM relationships and manufacturing infrastructure, meaning SSB technology adoption could accelerate through existing supply chains rather than requiring completely new ones.

Solid-state batteries will enter the premium vehicle market between 2027 and 2029 — not in mass-market vehicles. The first applications will be in ultra-premium EVs where a $15,000–$20,000 battery pack premium is absorbed into a $120,000+ vehicle price. Cost reduction follows scale; scale follows initial adoption. By 2032, SSBs will likely be competitive with lithium-ion on a total cost basis in mainstream segments. That's when the EV affordability crisis truly starts to resolve.

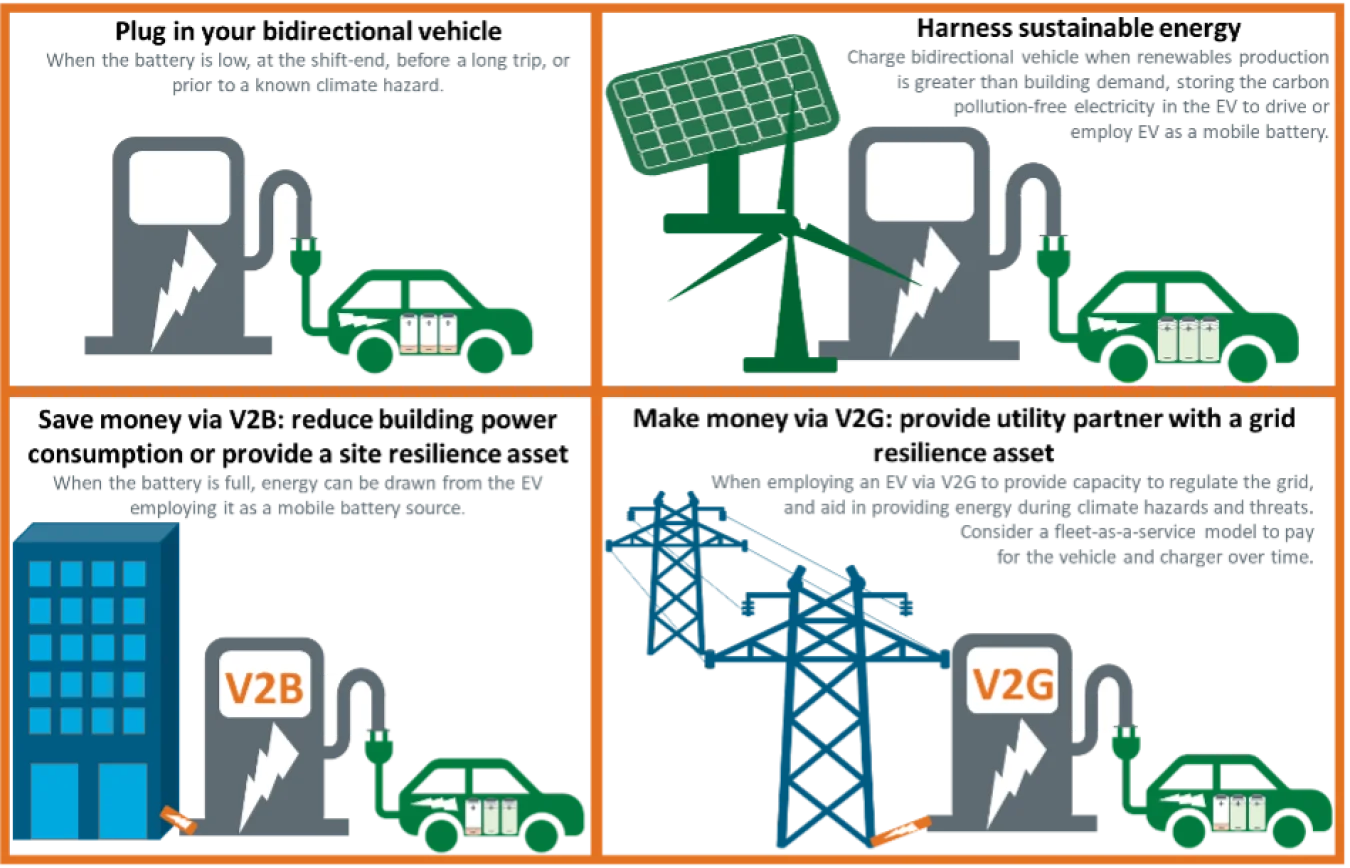

This is the most underrated trend in the entire automotive space, and it has a simple premise: a 100 kWh EV battery pack can store enough energy to power the average American home for 3–4 days. Most of the time, your car is parked — doing nothing with that energy. Vehicle-to-Grid technology lets utilities tap that storage, and you get paid for it.

Rocky Mountain Institute's Vehicle-Grid Integration analysis estimates that a fully integrated V2G network of just 5% of the US EV fleet could provide 200 gigawatt-hours of dispatchable grid storage — equivalent to dozens of utility-scale battery installations, but with zero additional infrastructure cost to the grid operator. The vehicles already exist. The battery capacity is already there. The only missing piece is the bidirectional charging hardware and software integration.

Grid operators in California, Texas, and the UK are running active V2G pilot programs, paying EV owners $0.20–0.50 per kWh to export power during peak demand — rates that translate to $10–25 per session during grid emergencies. That's passive income from a parked car.

Ford built V2G-adjacent technology directly into the F-150 Lightning from launch, under the branding "Ford Intelligent Backup Power." The Lightning can power a home for up to three days during an outage through its Pro Power Onboard system. Ford's approach — home backup first, grid export second — is the commercially smart sequencing: solve the customer's immediate problem (power outages), then layer in grid monetization as infrastructure matures.

Nissan has operated V2G programs in Japan since 2013 — the longest-running real-world V2G deployment anywhere. The Nissan Leaf's CHAdeMO connector supports bidirectional charging, and Nissan has documented over 8,300 V2G-enabled homes in Japan participating in grid stabilization programs with utility partners. This is not theoretical. It is a working model.

Volkswagen Group announced bidirectional charging compatibility across its MEB platform vehicles (ID.4, ID.3, Audi Q4 e-tron) beginning in 2024 model years in European markets — representing millions of compatible vehicles available to V2G programs. The scale of MEB platform deployment means that V2G infrastructure investments in Europe immediately have a large addressable fleet to serve.

V2G is 2–3 years from becoming a meaningful consumer income stream in the US. The utility integration, rate structure approvals, and standardized bidirectional charging hardware (ISO 15118-20 enables smart charging and V2G via standard CCS connectors) are all converging.

By 2028, expect major utilities to offer V2G enrollment programs the way they offer solar buyback programs today. The car sitting in your driveway will generate a material credit on your electricity bill — and change the total cost of EV ownership calculation in ways that make today's affordability concerns look much less daunting.

Pull back and look at all ten trends together, and a single pattern emerges: the automotive industry is not simply electrifying. It is being rebuilt from first principles — in software architecture, business models, supply chains, competitive dynamics, and the fundamental value equation of vehicle ownership.

The EV correction (Trend 1) isn't a failure of electric technology; it's a price and infrastructure problem that solid-state batteries (Trend 9) and V2G income streams (Trend 10) will methodically solve. The Chinese OEM invasion (Trend 3) and tariff disruption (Trend 4) are accelerating supply chain restructuring that makes the industry more resilient — but at a short-term cost that feeds the affordability crisis (Trend 7). Software-defined vehicles (Trend 2) and AI co-pilots (Trend 8) are transforming what a vehicle actually is, enabling autonomous trucking (Trend 5) at commercial scale while the EV startup shakeout (Trend 6) separates companies with real operational capability from those that only had compelling pitch decks.

The companies that will define automotive over the next decade share one characteristic: they're making decisions based on what's actually true in 2026, not on what the models predicted in 2021. The survivors — whether legacy OEMs, Chinese challengers, or the handful of startups still standing — are the ones who recalibrated fast enough when reality diverged from the forecast.

If you're building a business strategy, an investment thesis, or a career in or adjacent to automotive, the single most useful mental model is this: the car is becoming infrastructure. Infrastructure for mobility, yes — but also for energy storage, for software services, for data, and for AI training at a scale no other device can match. The companies that understand this earliest will build the most durable positions. The ones still thinking in terms of "vehicle sales" alone will find themselves increasingly irrelevant to the industry being built around them.

Want to spot emerging automotive and mobility trends before they hit mainstream? Check out our guide on how to identify market trends or explore what's gaining traction on our trends dashboard.

Thousands of Emerging Trends

Thousands of Breakout Apps

Mega Trends

Trend Analysis Tool